What is Attainable Housing and How Do We Return to the 1950's Mantra of "Housing for Everyone!”?

|

What is Attainable Housing and How Do We Return to the 1950's Mantra of "Housing for Everyone!”?

In some areas Attainable Housing is defined as Housing that can be afforded by someone earning the median family income in their community and where their mortgage and taxes and insurance payments do not exceed 30% of their gross monthly income. Others will set the bar at families with 80% of Area Median Income (AMI) Let’s look at a brief history of housing in America for a few moments. First off, in 1950, the average home constructed was 983 SF in 1955, yet today (2018 data) we construct single family detached homes that average about 2,344 SF for a Single family Detached (“SFD”) home (http://eyeonhousing.org/2018/08/new-single-family-home-size-continues-downward-trend/) |

NO WONDER we are having a problem building houses that are attainable to the average family!!!!

The average family size in 1950 was 3.54 according the U.S. Census Bureau.

(https://www.census.gov/population/socdemo/hh-fam/tabHH-6.pdf) In 2018 the average family size was just 2.53!!

We can no longer build "Average Houses" in 2019 that are over 138% larger than the "American Dream homes of 1950 and expect for families within 20% on either side of Median Family Incomes to even have a chance at ever owning one.

The simple math shows that it is unsustainable to achieve any affordable housing goal without right-sizing the product we build in our attainable housing communities. If we have family sizes that are fully one person per family smaller (39% difference) than 70 years ago, why are building homes that are on average 245% larger than the average homes of the Baby Boom Era?

The average Sales Price of a new Single-Family Detached (“SFD”) Home in 2018 4Q in Denver, CO was $568,312. If this home is 245% larger than necessary using 1950 data, then this results in this equation:

2018 SFD Average Price - $568,312

Size Factor – 245% or 2.45

$568,312 / 2.45 = $231, 964

The average family size in 1950 was 3.54 according the U.S. Census Bureau.

(https://www.census.gov/population/socdemo/hh-fam/tabHH-6.pdf) In 2018 the average family size was just 2.53!!

We can no longer build "Average Houses" in 2019 that are over 138% larger than the "American Dream homes of 1950 and expect for families within 20% on either side of Median Family Incomes to even have a chance at ever owning one.

The simple math shows that it is unsustainable to achieve any affordable housing goal without right-sizing the product we build in our attainable housing communities. If we have family sizes that are fully one person per family smaller (39% difference) than 70 years ago, why are building homes that are on average 245% larger than the average homes of the Baby Boom Era?

The average Sales Price of a new Single-Family Detached (“SFD”) Home in 2018 4Q in Denver, CO was $568,312. If this home is 245% larger than necessary using 1950 data, then this results in this equation:

2018 SFD Average Price - $568,312

Size Factor – 245% or 2.45

$568,312 / 2.45 = $231, 964

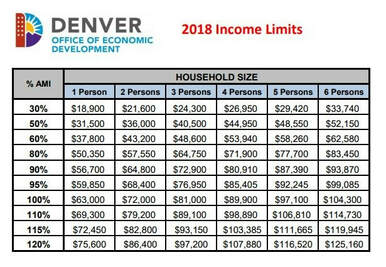

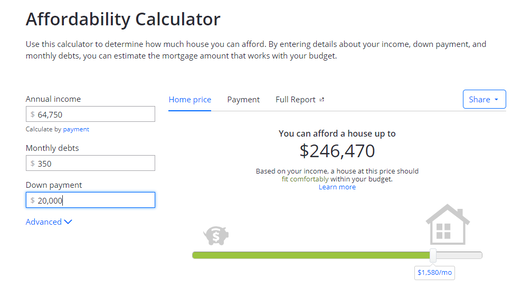

The next figure shows what a family making the Average Median Income (“AMI”) in Denver can afford with a $64,500 annual income and reasonable credit and a nominal down payment. Household debt in this example is low, at $350 per month for credit cards and auto payments. But certainly, a family of three could afford our imaginary attainable home if it were around $232,00 as shown in the numbers above and the assumptions in the table below:

Well, looky here, we solved the problem in one step!!!!!! …………. Oh wait, it’s never that easy, is it?

You can’t just reduce the size of the house to reduce the cost proportionately. ALL other factors in building a house must be reduced by the same factor for this magic equation to become a reality.

What are the other Costs in building a house besides Sticks and Bricks?

Lot size - The median lot size of a new single-family detached home sold in 2017 stands at 8,560 square feet, or just under one-fifth of an acre. In Denver, the average Lot size is under 5,000 SF. Reducing average lot size by this 245% ratio is not possible with existing zoning/planning laws in most areas of the Denver Market. 5,000 / 2.45 = 2,041. Minimum lot sizes range from 3,000 – 5,000 in most Denver metro area and other front range suburban communities.

However, that is just the tip of the iceberg, it can cost between $30,000 to 65,000 just to develop a lot in a master planned subdivision these days. How do we reduce that cost to $12,245 to $26,530. Well, therein lies the rub. You can’t reduce streets by a factor of 2.45. The average residential road is 30-36 feet wide and has sidewalks on both sides. Reducing by our 245% factor means reducing road widths to 12.25’ to 14.69’ – NOT GONNA HAPPEN!

You can’t just reduce the size of the house to reduce the cost proportionately. ALL other factors in building a house must be reduced by the same factor for this magic equation to become a reality.

What are the other Costs in building a house besides Sticks and Bricks?

Lot size - The median lot size of a new single-family detached home sold in 2017 stands at 8,560 square feet, or just under one-fifth of an acre. In Denver, the average Lot size is under 5,000 SF. Reducing average lot size by this 245% ratio is not possible with existing zoning/planning laws in most areas of the Denver Market. 5,000 / 2.45 = 2,041. Minimum lot sizes range from 3,000 – 5,000 in most Denver metro area and other front range suburban communities.

However, that is just the tip of the iceberg, it can cost between $30,000 to 65,000 just to develop a lot in a master planned subdivision these days. How do we reduce that cost to $12,245 to $26,530. Well, therein lies the rub. You can’t reduce streets by a factor of 2.45. The average residential road is 30-36 feet wide and has sidewalks on both sides. Reducing by our 245% factor means reducing road widths to 12.25’ to 14.69’ – NOT GONNA HAPPEN!

The Answer is Density!!!!!

The average city block size within the City and County of Denver and inner core suburbs on a gridded block is 1/8 of a mile north-south and 1/16 of a mile east west. That is 660 feet by 330 feet or 217,800 SF, or 5 acres. A typical urban grid block will have 20-24 homes on it. Using the mean, 22 homes, the density of this block is 22/5 acres or 4.4 per acre on a gross basis, as these measurements include the dimensions to the center lines of the streets. This is an important density factor, GROSS density -the total acreage divided by the Total number of homes provided. Including the roads is important because in developing land, almost 98% of the cost of construction is in the street ROW – Sidewalks, pavement, curb and gutter,Storm sewer, Sanitary sewer, Water Supply, other utilities, etc.

|

Since we can’t narrow the streets by 245% how can we increase the density of the city block? Accessory Dwelling Units (“ADU”) and Legal Basement Apartments!!! To get from 22 to 245% of 22 we need to get to nearly 54 units per lot - that’s an ADU on all 22 lots PLUS legal Basement Apartments . That’s pretty dense, probably not what inner core neighborhoods should all look like. And there is this…….Oh WAIT, what about traffic? Won’t the roads be clogged with twice as many cars?

|

TRANSIT ORIENTED DEVELOPMENT

OK, what about TRANSIT? – Dense urban cities have GREAT Transit! Denver has mediocre transit at Best. Bus lines are not effective in cross town commutes, so people still need cars. Our light rail system and bus interconnections are improving, but we are nowhere near the streets of Tokyo, New York City, Chicago and London. It is imperative that not only urban corridors have better transit, but also inner core suburbs as well. Transit only works where there is density, and the only way to achieve density is to have better transit!!! Sounds like conundrum or certainly an oxymoron. But it doesn’t have to be.

What about Transit Oriented Development (“TOD”)? Well, TOD’s sound great because you put the highest density housing right next to the Transit stops and you solve all the problems with density and transit being in the same place, RIGHT?

Not so fast, Urban Planners! I have been a huge proponent of TOD housing and mixed-use communities for several decades now but the most glaring factor to me is the cost of densdit as far as vertical construction is concerned. Podium Buildings, a very common Urban Architectural form used for Condominiums, Apartments and Mixed-Use developments is one of the most expensive types of residential construction. This type of construction can range in cost from $175 to $325 per square foot for just sticks and bricks. For our mythical 985 SF home, that cost is $172,375 - $320,125 just for the apartment, not including common space allocations and parking structure costs. A recent apartment building sale in Glendale (https://businessden.com/2019/01/07/glendale-apartment-complex-sells-for-108m/), the Podium-style apartments at AMLI Cherry Creek, with 341 units, sold for $108,000,000, making the deal worth about $317,000 a unit. This type of construction is not only valuable, but expensive to build. There used to be a time to convert apartments to affordable condominiums, but now that everyone is building luxury apartments, the only chance for attainable housing in condo conversions is going to come from dilapidated 1950’s style poorly maintained apartment buildings of 5-35 units sprinkled all over the metro area. But wait, won’t this displace lower income renters as well? Gentrification happens in many ways, and yes, this is one of them.

Construction Cost Case in Point -The Colorado Community Land Trust (“CCLT”) Homes within the Lowry Community in Denver. The Lowry Redevelopment Authority contracted with Builders to construct “attainable” workforce housing in several neighborhoods within the Lowry . one of these builders Writer Homes/Standard Pacific, contracted with Lowry for roughly $80/SF to construct 128 homes in Maple Park, a low density suburban townhouse style project on the east side of Lowry. There is no light rail Transit nearby, but this site sits along Lowry Boulevard, which has several buses running on commuter schedules right by the front door of the neighborhood. This is a fantastic solution, low cost housing types, constructed on lower cost land in the inner core, (not in the middle of a high priced TOD site), but with fantastic bus service. The $80/SF number is just for the vertical construction, but is clearly a better $280$ better, actually) alternative than Podium-style building that need MASSIVE government cash subsidies to get built and offered to affordable or attainable home buyers. Further, a willing developer, the LRA, and a willing partner, Standard Pacific Homes, constructed the site with limited subsidy from government, about $300,000 in State grants.

Maybe private developers CAN actually build these types of projects without government money?

Let’s see, what is the last piece?

– oh yeah government!!!! How can the government help with privately funded and developed attainable housing?

What about Transit Oriented Development (“TOD”)? Well, TOD’s sound great because you put the highest density housing right next to the Transit stops and you solve all the problems with density and transit being in the same place, RIGHT?

Not so fast, Urban Planners! I have been a huge proponent of TOD housing and mixed-use communities for several decades now but the most glaring factor to me is the cost of densdit as far as vertical construction is concerned. Podium Buildings, a very common Urban Architectural form used for Condominiums, Apartments and Mixed-Use developments is one of the most expensive types of residential construction. This type of construction can range in cost from $175 to $325 per square foot for just sticks and bricks. For our mythical 985 SF home, that cost is $172,375 - $320,125 just for the apartment, not including common space allocations and parking structure costs. A recent apartment building sale in Glendale (https://businessden.com/2019/01/07/glendale-apartment-complex-sells-for-108m/), the Podium-style apartments at AMLI Cherry Creek, with 341 units, sold for $108,000,000, making the deal worth about $317,000 a unit. This type of construction is not only valuable, but expensive to build. There used to be a time to convert apartments to affordable condominiums, but now that everyone is building luxury apartments, the only chance for attainable housing in condo conversions is going to come from dilapidated 1950’s style poorly maintained apartment buildings of 5-35 units sprinkled all over the metro area. But wait, won’t this displace lower income renters as well? Gentrification happens in many ways, and yes, this is one of them.

Construction Cost Case in Point -The Colorado Community Land Trust (“CCLT”) Homes within the Lowry Community in Denver. The Lowry Redevelopment Authority contracted with Builders to construct “attainable” workforce housing in several neighborhoods within the Lowry . one of these builders Writer Homes/Standard Pacific, contracted with Lowry for roughly $80/SF to construct 128 homes in Maple Park, a low density suburban townhouse style project on the east side of Lowry. There is no light rail Transit nearby, but this site sits along Lowry Boulevard, which has several buses running on commuter schedules right by the front door of the neighborhood. This is a fantastic solution, low cost housing types, constructed on lower cost land in the inner core, (not in the middle of a high priced TOD site), but with fantastic bus service. The $80/SF number is just for the vertical construction, but is clearly a better $280$ better, actually) alternative than Podium-style building that need MASSIVE government cash subsidies to get built and offered to affordable or attainable home buyers. Further, a willing developer, the LRA, and a willing partner, Standard Pacific Homes, constructed the site with limited subsidy from government, about $300,000 in State grants.

Maybe private developers CAN actually build these types of projects without government money?

Let’s see, what is the last piece?

– oh yeah government!!!! How can the government help with privately funded and developed attainable housing?

The Answer is to GET out of the WAY!!!

How could Lowry Redevelopment have not needed a $300,000 grant from the government to construct Maple Park? Well, let’s see, $300K is just about $2,344 per home. What could government do to get out of the way? Density bonuses come to mind, reduced fees come to mind? Expedited processing comes to mind (interest is a large part of any development’s overall budget and time is money) Water System development fees were already owned by the LRA as part of the base closure process and were donated by the LRA to the project. What if the Denver Water Board had provided a private developer a 50%

OK, local governments. How do we get back to where we came from? Some cities have actually tasked themselves with studying not only subsidized “Affordable Housing” but also “Attainable Housing”

Golden, Longmont and Denver are three examples.

GOLDEN

According to the City of Golden, Staff, Planning Commission, City Council and members of the community have been exploring the various regulatory options that would be viable for Golden. A significant existing regulatory barrier is the administrative process for distributing residential growth management allocations.

When it comes to attainable and affordable housing, in addition to adopting supportive policies and establishing goals, local governments may use their regulatory authority to:

· Remove existing barriers

· Create incentives

· Require participation

From the “We look forward to community conversations about these options as well as additional ideas that residents may have for supporting diverse and attainable housing in the community. Please feel free to contact staff at any time or to join us at any of the scheduled open house discussions.”

LONGMONT

From the Workforce Housing Task Force Recommendations from City of Longmont:

(Loacated here: https://www.longmontcolorado.gov/home/showdocument?id=9502 )

Values:

Housing in Longmont should continue to be available to all socio-economic levels so those who work in Longmont can choose to live in Longmont. Both the community and the individual benefit from people who both live and work in the community. Residents use local services, pay local taxes and support local businesses while experiencing lower commuting costs and greater housing choice.

• Housing regulations must be market sensitive in a way that encourages development of a range of housing choices in response to community needs as well as economic fluctuations.

• Government, non-profit and private for-profit entities involved in housing should continue to work collaboratively to support affordable housing needs and avoid duplication and overlap of services and programs.

• Longmont’s Comprehensive Plan must maintain a good balance between jobs and housing that meet the diverse needs of the community

• Longmont’s Comprehensive Plan must factor in social, economic and environmental variables that will lead to a sustainable future for all of Longmont’s residents. Housing that is affordable is a key component to a community wellbeing and long term sustainability.

• The City will ensure all affordable housing programs developed will contain a section that clearly states the goal and process for each program to Longmont’s community.

OK, local governments. How do we get back to where we came from? Some cities have actually tasked themselves with studying not only subsidized “Affordable Housing” but also “Attainable Housing”

Golden, Longmont and Denver are three examples.

GOLDEN

According to the City of Golden, Staff, Planning Commission, City Council and members of the community have been exploring the various regulatory options that would be viable for Golden. A significant existing regulatory barrier is the administrative process for distributing residential growth management allocations.

When it comes to attainable and affordable housing, in addition to adopting supportive policies and establishing goals, local governments may use their regulatory authority to:

· Remove existing barriers

· Create incentives

· Require participation

From the “We look forward to community conversations about these options as well as additional ideas that residents may have for supporting diverse and attainable housing in the community. Please feel free to contact staff at any time or to join us at any of the scheduled open house discussions.”

LONGMONT

From the Workforce Housing Task Force Recommendations from City of Longmont:

(Loacated here: https://www.longmontcolorado.gov/home/showdocument?id=9502 )

Values:

Housing in Longmont should continue to be available to all socio-economic levels so those who work in Longmont can choose to live in Longmont. Both the community and the individual benefit from people who both live and work in the community. Residents use local services, pay local taxes and support local businesses while experiencing lower commuting costs and greater housing choice.

• Housing regulations must be market sensitive in a way that encourages development of a range of housing choices in response to community needs as well as economic fluctuations.

• Government, non-profit and private for-profit entities involved in housing should continue to work collaboratively to support affordable housing needs and avoid duplication and overlap of services and programs.

• Longmont’s Comprehensive Plan must maintain a good balance between jobs and housing that meet the diverse needs of the community

• Longmont’s Comprehensive Plan must factor in social, economic and environmental variables that will lead to a sustainable future for all of Longmont’s residents. Housing that is affordable is a key component to a community wellbeing and long term sustainability.

• The City will ensure all affordable housing programs developed will contain a section that clearly states the goal and process for each program to Longmont’s community.

DENVER

On Monday, April 22, 2019, The Denver City Council passed the final “BluePrint Denver” as a supplement to “Denver’s Comprehensive Plan 2040”. Key details of the Comprehensive Plan focus on historic preservation of neighborhoods as the city continues to grow, and include an emphasis on planning for climate change in terms of water conservation, emergency planning, and more. Sarah Showalter, citywide planning supervisor with the City and County of Denver, told City Council that the most important aspect of Denver’s Comprehensive Plan 2040, and the part on which they received the most community feedback, was the “equitable, affordable, and inclusive” aspect. This refers to “the ability for everyone who wants to live here to do so,” Showalter said Monday night.

Sources: (https://www.5280.com/2019/04/denver-officially-has-a-blueprint-for-the-next-20-years-of-growth/”)

Read the Blueprint Denver plan here: https://www.denvergov.org/media/denvergov/cpd/blueprintdenver/Blueprint_Denver_City_Council_Draft.pdf

In the BluePrint Denver document, the dated term, “Affordable”, appears over 50 times, yet the the word “Attainable”, which has been adopted by the development community as a more important goal of providing market-based housing solutions for moderate income families, only appears twice. The preamble to the affordable housing section is good, and many ideas follow it. The opening paragraph reads:

“The following policies and strategies provide guidance on how land use and zoning regulations could provide more housing choice throughout the city. This includes diversifying housing options in new and existing neighborhoods as well as preserving and developing affordable housing. Denver is a diverse city and our housing types should accommodate the entire spectrum of housing needs, including quality options for vulnerable populations, attainable homeownership, non-traditional living arrangements, aging in place and intergenerational housing. These recommendations also direct growth to areas where new housing is closely linked to services and quality transportation.”

The two best parts of BluePrint Denver, if followed and implemented, could make Denver the best place for achieving attainable housing goals:

First:

“As housing needs throughout Denver have changed, city regulations have not kept pace with innovations including tiny home villages, intergenerational living, flexible living arrangements, and the changing needs and composition of households.”

And, Second:

“The “missing middle” refers to housing types that fall between high-density and single-unit houses, including duplexes, fourplexes, row homes, townhomes and cottage housing. Missing middle is not just the type of housing— it captures units that are attainable to middle-income households who still struggle to afford housing in Denver.”

With these two ideas put into action, Denver will be well on its way to becoming a VERY nice place to LIVE, not only for the Gentry and newcomers, but for young kids who go off to college and return to take jobs and raise there families, as well as immigrants who settle here for opportunity and the “American Dream”.

On Monday, April 22, 2019, The Denver City Council passed the final “BluePrint Denver” as a supplement to “Denver’s Comprehensive Plan 2040”. Key details of the Comprehensive Plan focus on historic preservation of neighborhoods as the city continues to grow, and include an emphasis on planning for climate change in terms of water conservation, emergency planning, and more. Sarah Showalter, citywide planning supervisor with the City and County of Denver, told City Council that the most important aspect of Denver’s Comprehensive Plan 2040, and the part on which they received the most community feedback, was the “equitable, affordable, and inclusive” aspect. This refers to “the ability for everyone who wants to live here to do so,” Showalter said Monday night.

Sources: (https://www.5280.com/2019/04/denver-officially-has-a-blueprint-for-the-next-20-years-of-growth/”)

Read the Blueprint Denver plan here: https://www.denvergov.org/media/denvergov/cpd/blueprintdenver/Blueprint_Denver_City_Council_Draft.pdf

In the BluePrint Denver document, the dated term, “Affordable”, appears over 50 times, yet the the word “Attainable”, which has been adopted by the development community as a more important goal of providing market-based housing solutions for moderate income families, only appears twice. The preamble to the affordable housing section is good, and many ideas follow it. The opening paragraph reads:

“The following policies and strategies provide guidance on how land use and zoning regulations could provide more housing choice throughout the city. This includes diversifying housing options in new and existing neighborhoods as well as preserving and developing affordable housing. Denver is a diverse city and our housing types should accommodate the entire spectrum of housing needs, including quality options for vulnerable populations, attainable homeownership, non-traditional living arrangements, aging in place and intergenerational housing. These recommendations also direct growth to areas where new housing is closely linked to services and quality transportation.”

The two best parts of BluePrint Denver, if followed and implemented, could make Denver the best place for achieving attainable housing goals:

First:

“As housing needs throughout Denver have changed, city regulations have not kept pace with innovations including tiny home villages, intergenerational living, flexible living arrangements, and the changing needs and composition of households.”

And, Second:

“The “missing middle” refers to housing types that fall between high-density and single-unit houses, including duplexes, fourplexes, row homes, townhomes and cottage housing. Missing middle is not just the type of housing— it captures units that are attainable to middle-income households who still struggle to afford housing in Denver.”

With these two ideas put into action, Denver will be well on its way to becoming a VERY nice place to LIVE, not only for the Gentry and newcomers, but for young kids who go off to college and return to take jobs and raise there families, as well as immigrants who settle here for opportunity and the “American Dream”.

OTHER GOVERNMENT SOLUTIONS

Although Denver proper has committed millions in cash subsidies for affordable housing solutions and approved a wonderful plan for the future, other municipalities would be wise to follow suit and institute other solutions for Government assistance without providing direct cash subsidies:

Reduce government fees

Water Taps – Water usage in a home is a factor of many things, family size, number of bathrooms, size of the landscaped area, number of plumbing fixtures. Attainable housing can be achieved when Water Utilities and municipalities apply these factors to their rates.

Building Permits and Zoning/Planning Plan Requirements – Sometimes many htousands of dollars of investments, just in the engineering and architectural plans are required to add new uses to an existing home or building in municipalities throughout Denver. A recent client of Millennium Development Solutions was unable to afford nearly $25,000 per unit in such costs to simply follow the new “Main Street Zoning” requirements for the Old Aurora Zoning Overlay District that was approved in 2018 as a tool to increase neighborhood density and create affordable housing solutions in Old Aurora along East Colfax between Peoria St. and Yosemite St.

Reduce government Interference

Zoning – Allow smaller homes, Allow Smaller lots, Allow Accessory Dwelling units, allow higher density in areas of change where larger, older homes exist so apartments and condominiums can be created in homes that millennials and Gen Z’s will probably never buy from their grandparents.

Mixed-Income communities should be encouraged, as it is easier for developers of large-scale projects to include smaller lots to accommodate the needs of younger working families within much larger neighborhoods. Segregating wealth by neighborhood should be a thing of the past. Habitat for Humanity and Community Land Trusts should be able build homes right next door to $500,000 to $1,000,000 homes on land provided by the developers at reduced rates or even for free.

Review and processing times-

Building departments have become payers of bureaucracy for ALL developers, but priority in progressive communities should be given to those developers who work to achieve attainable housing goals. Fast track approval systems have been used in other cities with success to help developers of workforce housing, affordable housing and attainable housing.

Provide Free or Reduced Price Government Land -

When governments, both local (municipalities, counties and school districts) have excess land, they should make it available to attainable and affordable housing developers at a sliding scale, the providers of homeless housing solutions should get land for free, and then based on the AMI levels served, land should be discounted on a sliding scale based on the level of AMI served by the developer. Also, State government owns Millions acres, I need not say more about that aspect……

Reduce government fees

Water Taps – Water usage in a home is a factor of many things, family size, number of bathrooms, size of the landscaped area, number of plumbing fixtures. Attainable housing can be achieved when Water Utilities and municipalities apply these factors to their rates.

Building Permits and Zoning/Planning Plan Requirements – Sometimes many htousands of dollars of investments, just in the engineering and architectural plans are required to add new uses to an existing home or building in municipalities throughout Denver. A recent client of Millennium Development Solutions was unable to afford nearly $25,000 per unit in such costs to simply follow the new “Main Street Zoning” requirements for the Old Aurora Zoning Overlay District that was approved in 2018 as a tool to increase neighborhood density and create affordable housing solutions in Old Aurora along East Colfax between Peoria St. and Yosemite St.

Reduce government Interference

Zoning – Allow smaller homes, Allow Smaller lots, Allow Accessory Dwelling units, allow higher density in areas of change where larger, older homes exist so apartments and condominiums can be created in homes that millennials and Gen Z’s will probably never buy from their grandparents.

Mixed-Income communities should be encouraged, as it is easier for developers of large-scale projects to include smaller lots to accommodate the needs of younger working families within much larger neighborhoods. Segregating wealth by neighborhood should be a thing of the past. Habitat for Humanity and Community Land Trusts should be able build homes right next door to $500,000 to $1,000,000 homes on land provided by the developers at reduced rates or even for free.

Review and processing times-

Building departments have become payers of bureaucracy for ALL developers, but priority in progressive communities should be given to those developers who work to achieve attainable housing goals. Fast track approval systems have been used in other cities with success to help developers of workforce housing, affordable housing and attainable housing.

Provide Free or Reduced Price Government Land -

When governments, both local (municipalities, counties and school districts) have excess land, they should make it available to attainable and affordable housing developers at a sliding scale, the providers of homeless housing solutions should get land for free, and then based on the AMI levels served, land should be discounted on a sliding scale based on the level of AMI served by the developer. Also, State government owns Millions acres, I need not say more about that aspect……

CONCLUSION

This is not an easy task. Attainable housing is a very multi-faceted and complex issue, It is a perfect example of a Public-Private Partnership where the Cities, State, School Boards, Water Boards, and other governmental entities can all work with private developers without paying one cent in cash subsidy. Let the Free Markets pull developers who are passionate about this crisis within our communities and join forces with municipalities to provide attainable housing at a rate never seen before by using many of these ideas, not all will work in every area, and shouldn’t be mandated of all who play in the real estate development game. (New Jersey’s affordable program, as a result of the landmark Mt Laurel court cases, was fraught with the failed principle of jamming affordable housing into every single community in the state.) Now why on Earth would Cherry Hills Village want attainable housing, it’s a premier luxury community, one of the finest in the nation, and the people who live there like their privacy and comfort of large lots and voluminous homes.

Attainable housing doesn’t have to be a goal of EVERY community, but every community should be aware of what they are doing that prevents working families from being able to live and work in the same area. No need to bus people in from the suburbs to be janitors downtown when we have such great thinkers and doers within both our governments and our private real estate community. I look forward to community conversations about these options as well as additional ideas that residents may have for supporting diverse and attainable housing in the community. Please feel free to contact me at any time or to join this movement of thoughtful and engaged community developers who are passionate about "Attainable Housing"

John Ewing can be reached at 720-505-1875 or though the Millennium Development Solutions' website at http://www.millenniumdevelopmentsolutions.com/index.html

This Article was published on Linkedin on April 25, 2019

Attainable housing doesn’t have to be a goal of EVERY community, but every community should be aware of what they are doing that prevents working families from being able to live and work in the same area. No need to bus people in from the suburbs to be janitors downtown when we have such great thinkers and doers within both our governments and our private real estate community. I look forward to community conversations about these options as well as additional ideas that residents may have for supporting diverse and attainable housing in the community. Please feel free to contact me at any time or to join this movement of thoughtful and engaged community developers who are passionate about "Attainable Housing"

John Ewing can be reached at 720-505-1875 or though the Millennium Development Solutions' website at http://www.millenniumdevelopmentsolutions.com/index.html

This Article was published on Linkedin on April 25, 2019

Baby Boomers to Continue to Affect Housing,

Just in a Different Way

Originally Published on LinkedIn Pulse - July 14, 2015. Click on Photo for Link.

Originally Published on LinkedIn Pulse - July 14, 2015. Click on Photo for Link.

The 76 million Americans born between 1946 and 1964, the baby-boom generation, have affected American culture for decades, especially trends within the Housing Industry. Whether propelling social change, or driving the economy, the "Boomers" will continue to affect our way of life for another several decades. A wave of retirements among Boomers in the decades to come will have a increasing impact on residential real estate, in ways that are toppling some conventional assumptions. Housing decisions that loom for this generation are numerous. Retirements have been delayed by the recent economic downturn, Boomers are working longer and are healthier than their parents, and will continue to be involved in their children's lives. Each of these facts will affect housing and builders and developers need to be mindful of these dynamics.

Many Boomers are expected to struggle to afford their existing homes in retirement as they continue to face large mortgage burdens and a limited income, according to a report by the Harvard Joint Center for Housing Studies and the AARP Foundation. Combined with less savings and more household debt than the "Greatest Generation" before them, finances will drive most of their housing decisions moving forward. Also, within the next 10 years, the percentage of households age 65 and older who are living on less than $15,000 a year -- considered below the poverty line for a two-person household – is expected to increase by nearly 40 percent, according to the report. The broad differences between incomes and current housing conditions will develop a variety of branches in the housing tree, some which are tried and true, and some which have not yet been tried at all.

First, let's look at the Boomers who have it all now, and are wondering what to do next. Big McMansions exist in every community across the US, but will Boomers be able to sell them to the generations following them - the Gen Xers and Millennials? A vast majority of today’s households with children still want such houses, Nelson says. But about a quarter of them want something else, like condos and urban townhouses. That demand, which barely existed just a decade ago, is now nearly a quarter of the market. Even with some demand for this type of housing still continuing, there will certainly be a mismatch between supply and demand. Preferences of younger buyers will continue to evolve, and the demographics indicate their preferences will not match those of the supply of resales offered by the Boomers. Certainly, some Gen Xers will move on up and into these bigger homes, but most will opt for smaller housing options as their own families mature. Most Gen Xers are already settled, and many of the cohort (loosely defined as those born between 1961 and 1980) are plateauing in their careers, have the financial stress of raising families of their own, and now have also been hardest hit by the economic downturn. It's hard to convince a Gen Xer to buy a home that big now. Millennials are completely uninterested in buying something bigger than they need, so the dilemma for Boomers is to find a buyer for their larger homes quicker, rather than later, in their life cycle. If not, they might find a huge oversupply condition and lose substantial equity in a buyer's market for these larger homes.

Boomers who have suffered the most during the economic down cycles of 2000 and 2008 will be working longer before they finally retire, and will most likely have fewer options available to them at that time than the more successful members of the cohort. Many of these Boomer homeowners will become renters. Roughly 7 percent of over-65 households move each year, and as people get older, their likelihood of moving from owning to renting gets higher and higher (it’s about 79 percent for households over 85). By 2020, there were will be around 35 million over-65 households in the U.S. That year, researcher Arthur C. Nelson calculates, seniors who would like to become renters will be trying to sell about 200,000 more owner-occupied homes than there will be new households entering the market to buy them. By 2030, that figure could rise to half a million housing units a year. This trend will need to be captured as perhaps a new sub-market by the apartment development community to attract and retain active seniors who prefer lifestyles different then the younger Millennial and Gen Xer renters.

What to do with my big old house? Several options exist in more established communities, but these solutions might not be available in newer, well laid out planned communities developed in the last 30-plus years due to zoning and Homeowner's Association covenants and restrictions. For some, aging in place will be the only option, and if their children are now living in other states, having that extra space will just translate to temporary, vacation and short-term housing for their children and grandchildren. For others, it’s time to further flex with creative housing solutions like condo conversions, boarding house conversions, co-housing, shared purchase of an apartment buildings. If they can’t get out of their current homes, Boomers need to consider radical renovations — to their houses and to their ways of life — that will allow them to age in place, bring new people into their homes, and generally start to live a little differently. These options will most likely consume just a small percentage of the market. This type of creativity is still in its infancy, and even more options might develop in established communities across the US. Communities that are growing, like sunbelt metros like Dallas, Phoenix, Charlotte, and Atlanta will still see huge demand from younger families and will be less affected by exiting/arriving Boomer than areas that are shrinking or undergoing other demographic changes.

The other huge impact will be on the retirement community market. As more empty nester couples age in place and work farther past retirement ages, demand for strictly retirement style communities will lessen. As the greatest generation continues to die off and leave these retirement lifestyle communities that were created when they first retired. This changing demand will result in fewer new starts and perhaps a flattening of prices within communities that have predominantly retirement homes as in Sun City, AZ and the myriad of Florida markets currently supporting this lifestyle. A study of Lehigh Valley. PA retirees showed that Lehigh Valley's baby boomers, like their cohorts across the country, are less likely than previous generations to head towards a retirement of shuffleboard among the palm trees. Nor are they necessarily flocking to the traditional facilities that can carry them through the tiers of the senior years, from the immediate post-retirement period all the way to nursing care. Those places — retirement-destination states and independent living communities — surely remain a vital part of the retirement landscape. But Boomers, with their Peter Pan-like resistance to the notion of growing old, have been driving the national demand for housing that allows them to "age in place." Developers and Builders are increasingly aware of this phenomena and are finding that aging communities can be easily served by new local planned developments that allow them to stay close to family and friends, but only if they can find buyers for their existing homes.

Baby boomers are not only working longer but also choosing “phased” retirements, in which they work at least part time after exiting their primary careers. This sub-group is changing the definition of a “retirement” locale, driving migration to cities with affordable housing, recreational opportunities in addition to robust economies that can support job growth. Sun Belt cities in Florida and Arizona satisfy these requirements in addition to locations like McAllen, TX, Boise, ID, Greenville, S.C., Chattanooga, Tenn.; and Raleigh, N.C. Housing in such places is relatively affordable and taxes are low. Such markets are attractive to Boomers, who are moving en masse toward retirement age but don’t necessarily want to stop working all at once. Downsizing housing options for this sub-group will include smaller homes in active, amenity-rich communities.

The "Great Senior Sell-Off" is not on our doorstep yet, but it might start to become a noticeable trend by the end of this decade. Certainly the market will be vastly different in 2020 through 2030 and our industry needs to be mindful today of these developing trends when doing long range forecasting and business planning. The Boomer generation's housing decisions as time moves on will need to be studied further and developing trends identified and monitored for the housing industry to adapt appropriately.

Many Boomers are expected to struggle to afford their existing homes in retirement as they continue to face large mortgage burdens and a limited income, according to a report by the Harvard Joint Center for Housing Studies and the AARP Foundation. Combined with less savings and more household debt than the "Greatest Generation" before them, finances will drive most of their housing decisions moving forward. Also, within the next 10 years, the percentage of households age 65 and older who are living on less than $15,000 a year -- considered below the poverty line for a two-person household – is expected to increase by nearly 40 percent, according to the report. The broad differences between incomes and current housing conditions will develop a variety of branches in the housing tree, some which are tried and true, and some which have not yet been tried at all.

First, let's look at the Boomers who have it all now, and are wondering what to do next. Big McMansions exist in every community across the US, but will Boomers be able to sell them to the generations following them - the Gen Xers and Millennials? A vast majority of today’s households with children still want such houses, Nelson says. But about a quarter of them want something else, like condos and urban townhouses. That demand, which barely existed just a decade ago, is now nearly a quarter of the market. Even with some demand for this type of housing still continuing, there will certainly be a mismatch between supply and demand. Preferences of younger buyers will continue to evolve, and the demographics indicate their preferences will not match those of the supply of resales offered by the Boomers. Certainly, some Gen Xers will move on up and into these bigger homes, but most will opt for smaller housing options as their own families mature. Most Gen Xers are already settled, and many of the cohort (loosely defined as those born between 1961 and 1980) are plateauing in their careers, have the financial stress of raising families of their own, and now have also been hardest hit by the economic downturn. It's hard to convince a Gen Xer to buy a home that big now. Millennials are completely uninterested in buying something bigger than they need, so the dilemma for Boomers is to find a buyer for their larger homes quicker, rather than later, in their life cycle. If not, they might find a huge oversupply condition and lose substantial equity in a buyer's market for these larger homes.

Boomers who have suffered the most during the economic down cycles of 2000 and 2008 will be working longer before they finally retire, and will most likely have fewer options available to them at that time than the more successful members of the cohort. Many of these Boomer homeowners will become renters. Roughly 7 percent of over-65 households move each year, and as people get older, their likelihood of moving from owning to renting gets higher and higher (it’s about 79 percent for households over 85). By 2020, there were will be around 35 million over-65 households in the U.S. That year, researcher Arthur C. Nelson calculates, seniors who would like to become renters will be trying to sell about 200,000 more owner-occupied homes than there will be new households entering the market to buy them. By 2030, that figure could rise to half a million housing units a year. This trend will need to be captured as perhaps a new sub-market by the apartment development community to attract and retain active seniors who prefer lifestyles different then the younger Millennial and Gen Xer renters.

What to do with my big old house? Several options exist in more established communities, but these solutions might not be available in newer, well laid out planned communities developed in the last 30-plus years due to zoning and Homeowner's Association covenants and restrictions. For some, aging in place will be the only option, and if their children are now living in other states, having that extra space will just translate to temporary, vacation and short-term housing for their children and grandchildren. For others, it’s time to further flex with creative housing solutions like condo conversions, boarding house conversions, co-housing, shared purchase of an apartment buildings. If they can’t get out of their current homes, Boomers need to consider radical renovations — to their houses and to their ways of life — that will allow them to age in place, bring new people into their homes, and generally start to live a little differently. These options will most likely consume just a small percentage of the market. This type of creativity is still in its infancy, and even more options might develop in established communities across the US. Communities that are growing, like sunbelt metros like Dallas, Phoenix, Charlotte, and Atlanta will still see huge demand from younger families and will be less affected by exiting/arriving Boomer than areas that are shrinking or undergoing other demographic changes.

The other huge impact will be on the retirement community market. As more empty nester couples age in place and work farther past retirement ages, demand for strictly retirement style communities will lessen. As the greatest generation continues to die off and leave these retirement lifestyle communities that were created when they first retired. This changing demand will result in fewer new starts and perhaps a flattening of prices within communities that have predominantly retirement homes as in Sun City, AZ and the myriad of Florida markets currently supporting this lifestyle. A study of Lehigh Valley. PA retirees showed that Lehigh Valley's baby boomers, like their cohorts across the country, are less likely than previous generations to head towards a retirement of shuffleboard among the palm trees. Nor are they necessarily flocking to the traditional facilities that can carry them through the tiers of the senior years, from the immediate post-retirement period all the way to nursing care. Those places — retirement-destination states and independent living communities — surely remain a vital part of the retirement landscape. But Boomers, with their Peter Pan-like resistance to the notion of growing old, have been driving the national demand for housing that allows them to "age in place." Developers and Builders are increasingly aware of this phenomena and are finding that aging communities can be easily served by new local planned developments that allow them to stay close to family and friends, but only if they can find buyers for their existing homes.

Baby boomers are not only working longer but also choosing “phased” retirements, in which they work at least part time after exiting their primary careers. This sub-group is changing the definition of a “retirement” locale, driving migration to cities with affordable housing, recreational opportunities in addition to robust economies that can support job growth. Sun Belt cities in Florida and Arizona satisfy these requirements in addition to locations like McAllen, TX, Boise, ID, Greenville, S.C., Chattanooga, Tenn.; and Raleigh, N.C. Housing in such places is relatively affordable and taxes are low. Such markets are attractive to Boomers, who are moving en masse toward retirement age but don’t necessarily want to stop working all at once. Downsizing housing options for this sub-group will include smaller homes in active, amenity-rich communities.

The "Great Senior Sell-Off" is not on our doorstep yet, but it might start to become a noticeable trend by the end of this decade. Certainly the market will be vastly different in 2020 through 2030 and our industry needs to be mindful today of these developing trends when doing long range forecasting and business planning. The Boomer generation's housing decisions as time moves on will need to be studied further and developing trends identified and monitored for the housing industry to adapt appropriately.

Millennials to Impact Homebuilding Industry for Decades

Originally Published on July 2, 2015 at LinkedIn Pulse. (Click on photo for link)

Originally Published on July 2, 2015 at LinkedIn Pulse. (Click on photo for link)

One of the largest generations in history is moving into its prime spending years. Millennials are poised to reshape the economy. Their unique experiences will change the ways we buy and sell homes, forcing builders and developers to examine how they do business for decades to come.

Millennials recently passed the Baby Boomers as the US's largest generation. While the impacts of the Boomers continue to be felt by the housing industry, the Millennials impacts are just beginning. Millennials are our first digital natives and have seemingly grown up in the midst of the most rapid changing economy of our lifetimes. Born between 1980 and 2000, they have a different set of priorities, and certainly have a different world view than their parents. Their expectations are vastly different than most other generations', and those expectations involve every aspect of their lives.

So far, the biggest impact this generation has had on the housing industry is in their unwillingness to settle down, first influencing the current boomlet in apartment construction. Once they begin household formations and start to have children and create more traditional families, their desire to buy single family homes in good neighborhoods will create another boom in this market segment. Trulia surveys estimate that 93% of Millennials aged 18-34 plan to buy a home some day, while only 39% of Boomers aged 55-plus plan on buying again. The sheer size of the cohort, 92,000,000 in the US alone, makes that a daunting market segment to reconcile with in the years to come.

Experts have been baffled by this group's propensity to live at home longer than any generation that preceded it. The peak years of births in this generation are 1990 and 1991, with 4.73 million birth each year. These 24-25 year olds are just entering the housing market and the group just older than them has shown some interesting characteristics. Goldman Sachs Global Investment Research has published that almost 30% of 18-34 year olds in 2010 still lived at home for part of the year. In 2001 that figure was closer to 27%. The Federal Reserve of New York reported that "while 30 year olds in 2003 were almost twice as likely to own a home (with some home-secured debt) as they were to live with their parents, owning and living with parents were equally likely for 30 year olds in 2013."

Mobility, massive student debt and lower paying jobs have so far kept these hipsters at home with parents and in apartments. The massive financial crisis in 2008 occurred when the peak of this generation was just starting college and it has certainly made an impact on the permanence of their decision making processes. Also, an ongoing increase in the age at first marriage in the U.S., coupled with an increase in cohabitation, has kept traditional household formation at bay. Most young couples express a desire to create traditional families, but wait longer to get married; therefore, the need for suburban lifestyle homes in neighborhoods with excellent schools has been delayed. In the coming decade, household formations by Millennials are expected to rise at rapid rates as they reach the prime ages of 25-34.. According to some forecasts, Millennials are expected to drive two-thirds of household formations over the next five years.

Design and style are important to Millennials. They have the internet to support their rapid data gathering when they begin to seek more permanent homes. They often don't seek professional help when they start their searches but rather first look for ideas for what’s chic online from resources such as Houzz, Pinterest, Instagram, Etsy, and retailers’ websites. And they tend to make decisions fast after sharing information with friends for feedback. "They often contact real estate and design professionals to validate their own choices, so the best way to work with them is to make them part of the process", says Chicago designer Tom Segal of Kaufman Segal Design. The interior layouts that attract Millennials come in all sorts of variations, but the "key is fewer partitions and walls since this group likes to socialize and live casually", says Larry Abbott, a remodeling and home improvement specialist in Houston. Many don’t want a formal living or dining room, says designer Shana Jacobs of MP Studio in Houston. Less, more efficient square footage will be in demand and multi-use spaces will also be popular. Workout equipment is not uncommon in the central living area for this group.

"Location, Location, Location" will continue to drive housing purchase decisions. For this generation, this still means living close to an urban core or transit, so they can easily reach services and their old friends and co-workers. Also, they tend to be more financially conservative than their parents and will put a larger percentage down to secure their mortgages, because they have fears of foreclosures as they saw their parents suffer in 2008-2010 by stretching too far. Many Millennials have dropped car ownership and have adopted ZipCar and Car2Go as their means of traveling outside of public transit corridors. Big 3-car garages may no longer be necessary for these carbon footprint conscious members of the new generation.

Every developer and homebuilder will have to adjust their homes and communities to accommodate Millennial preferences for the type of home in which they want to raise families. The end result will be more family-friendly neighborhoods where homes serve as the hub for their owner’s economic activity, simultaneously lowering the nation’s carbon footprint and hopefully improving the civic health of its communities.

By 2020 the Millennial generation will comprise more than one third of adult Americans (36%). The Millennial generation’s overwhelming size will place a lasting imprint on the nation’s housing market, just as their parents, the Baby Boomers, influenced the housing market when they started buying homes and raising families themselves.

Millennials recently passed the Baby Boomers as the US's largest generation. While the impacts of the Boomers continue to be felt by the housing industry, the Millennials impacts are just beginning. Millennials are our first digital natives and have seemingly grown up in the midst of the most rapid changing economy of our lifetimes. Born between 1980 and 2000, they have a different set of priorities, and certainly have a different world view than their parents. Their expectations are vastly different than most other generations', and those expectations involve every aspect of their lives.

So far, the biggest impact this generation has had on the housing industry is in their unwillingness to settle down, first influencing the current boomlet in apartment construction. Once they begin household formations and start to have children and create more traditional families, their desire to buy single family homes in good neighborhoods will create another boom in this market segment. Trulia surveys estimate that 93% of Millennials aged 18-34 plan to buy a home some day, while only 39% of Boomers aged 55-plus plan on buying again. The sheer size of the cohort, 92,000,000 in the US alone, makes that a daunting market segment to reconcile with in the years to come.

Experts have been baffled by this group's propensity to live at home longer than any generation that preceded it. The peak years of births in this generation are 1990 and 1991, with 4.73 million birth each year. These 24-25 year olds are just entering the housing market and the group just older than them has shown some interesting characteristics. Goldman Sachs Global Investment Research has published that almost 30% of 18-34 year olds in 2010 still lived at home for part of the year. In 2001 that figure was closer to 27%. The Federal Reserve of New York reported that "while 30 year olds in 2003 were almost twice as likely to own a home (with some home-secured debt) as they were to live with their parents, owning and living with parents were equally likely for 30 year olds in 2013."

Mobility, massive student debt and lower paying jobs have so far kept these hipsters at home with parents and in apartments. The massive financial crisis in 2008 occurred when the peak of this generation was just starting college and it has certainly made an impact on the permanence of their decision making processes. Also, an ongoing increase in the age at first marriage in the U.S., coupled with an increase in cohabitation, has kept traditional household formation at bay. Most young couples express a desire to create traditional families, but wait longer to get married; therefore, the need for suburban lifestyle homes in neighborhoods with excellent schools has been delayed. In the coming decade, household formations by Millennials are expected to rise at rapid rates as they reach the prime ages of 25-34.. According to some forecasts, Millennials are expected to drive two-thirds of household formations over the next five years.

Design and style are important to Millennials. They have the internet to support their rapid data gathering when they begin to seek more permanent homes. They often don't seek professional help when they start their searches but rather first look for ideas for what’s chic online from resources such as Houzz, Pinterest, Instagram, Etsy, and retailers’ websites. And they tend to make decisions fast after sharing information with friends for feedback. "They often contact real estate and design professionals to validate their own choices, so the best way to work with them is to make them part of the process", says Chicago designer Tom Segal of Kaufman Segal Design. The interior layouts that attract Millennials come in all sorts of variations, but the "key is fewer partitions and walls since this group likes to socialize and live casually", says Larry Abbott, a remodeling and home improvement specialist in Houston. Many don’t want a formal living or dining room, says designer Shana Jacobs of MP Studio in Houston. Less, more efficient square footage will be in demand and multi-use spaces will also be popular. Workout equipment is not uncommon in the central living area for this group.

"Location, Location, Location" will continue to drive housing purchase decisions. For this generation, this still means living close to an urban core or transit, so they can easily reach services and their old friends and co-workers. Also, they tend to be more financially conservative than their parents and will put a larger percentage down to secure their mortgages, because they have fears of foreclosures as they saw their parents suffer in 2008-2010 by stretching too far. Many Millennials have dropped car ownership and have adopted ZipCar and Car2Go as their means of traveling outside of public transit corridors. Big 3-car garages may no longer be necessary for these carbon footprint conscious members of the new generation.

Every developer and homebuilder will have to adjust their homes and communities to accommodate Millennial preferences for the type of home in which they want to raise families. The end result will be more family-friendly neighborhoods where homes serve as the hub for their owner’s economic activity, simultaneously lowering the nation’s carbon footprint and hopefully improving the civic health of its communities.

By 2020 the Millennial generation will comprise more than one third of adult Americans (36%). The Millennial generation’s overwhelming size will place a lasting imprint on the nation’s housing market, just as their parents, the Baby Boomers, influenced the housing market when they started buying homes and raising families themselves.

ULI Study Takes the Macro View on Micro Apartments

Excerpts from the study:Definition of Micro Unit: What exactly qualifies as a micro unit? A micro unit might be 300 square feet in New York City or 500 square feet in Dallas. This study learned that no standard definition exists. A micro unit is a somewhat ambiguous term that covers anything from a relatively small studio or one-bedroom apartment to a short-term lease, SRO unit with communal kitchen and common room areas. In fact, many in the industry are moving away from branding their units as micro because the term has begun to arouse negative connotations associated with higher density, overcrowding, and transient populations.

Ideal SizeIn an attempt to understand what constitutes the ideal size for a micro unit, one developer inter - viewed for this effort revealed that it had conducted some primary consumer research on the subject. The developer created a series of micro-unit mockups and had a graduate student live in the units and provide feedback on what worked and what did not. Based on this research, this developer determined that a micro unit with less than 200 square feet was too small, that a unit with 375 square feet was too large, and that something in the 275- to 300-square oot range was optimal for a “one person plus dog” household. This research also revealed the need to have flexible furniture systems and adequate storage for units this small to be workable.

Key Findings from historical data: Among the key findings from the historical data are the following:

1) In properties built during the 2012–2013 time frame, average unit size (950 square feet) is down nearly 50 square feet from the average recorded in the previous cycle (both early in that cycle and late in the cycle).

2) Although a tendency exists toward slight downsizing of units in one-bedroom configuration, the real driving force behind the smaller overall average unit size is a shift in the mix of floor plans offered, with more studio and one-bedroom units and fewer two-bedroom units and apartments with three or more bedrooms. The shift in unit mix corresponds to a greater share of development occurring in urban settings, where household size is smaller.

ConclusionsMicro units have generated considerable interest and some controversy in the real estate community in the past several years. This research illustrates that the migration toward smaller average unit size, based on a shift in mix to studio and one-bedroom units, and the number of rental apartment communities offering micro units are a growing trend. Whether this turns out to be a lasting phenomenon or a passing fad, micro units have renewed the focus on efficient layouts and innovative design solutions. Many of these smaller units are designed and configured to feel larger to potential renters than older conventional units by virtue of higher ceiling heights, larger windows, built-in storage, and in some cases, flexible furniture systems. The evidence from the market indicates that smaller units tend to outperform conventional units; they tend to have higher occupancy and achieve significant rent premiums. Still unclear is whether this performance is driven by the relatively limited supply of these smaller units on the market, or whether a sizable, and perhaps untapped, segment of renters is willing to make the tradeoff and pay considerably more per square foot rent in exchange for highly desirable locations, better community amenities, the ability to forgo a roommate—or perhaps some combination of these factors. The consumer research indicates that, from the renter’s perspective, the micro-unit strategy that offers a lower monthly rent “sticker price” compared with conventional units is a compelling proposition. But it is also clear from the research that micro units are not for everyone and that micro units may not be the solution for every location.

http://uli.org/wp-content/uploads/ULI-Documents/MicroUnit_full_rev_2015.pdf